Equity capital firms also target extremely high-growth business with substantial potential, i.e – tyler tysdal business. Web companies such as Facebook, Google, and other innovative technology companies in health care, renewable resource, biotech, and so on however that also have more possible to go bust! Hedge Funds purchase publicly noted securities and generally do not look for to get control of companies they purchase.

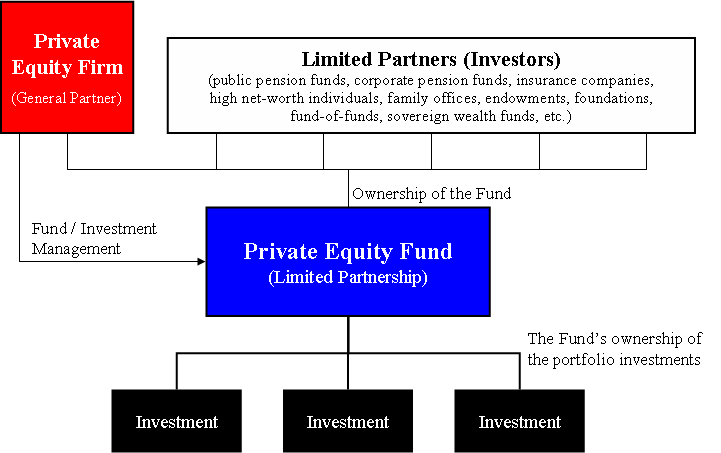

Wealthy individuals, pension funds, and shared funds are the typical investors in private equity funds. Due to the fact that LBO returns (typically 20-30% over four to five years) can only be achieved with a lot of financial obligation and good growth capacity, the target business need to be rather stable. So strong, specific niche, market-leading business with cost-cutting and expansion capacity in non-cyclical markets are favoured targets.

A number of these individuals originate from Oxbridge/Ivy League universities, typically with leading MBAs. Since firms are very small (10 to 20 individuals usually), there are very couple of tasks offered. Also, requirements are really high due to the high level of responsibility. This makes the market incredibly competitive, even far more than investment banking.

You can inspect our list of London-based PE funds Below is a list of the top hedge funds based in London. This list just includes the big hedge funds, with properties under management of at least over $1 billion. Note nevertheless that those hedge funds are a mix of macro funds, relative value, credit, equity long/short, multi-strategy, fixed-income, arbitrage, activist, bonds and so on. securities fraud racketeering.

Private Equity Firm Hierarchy And Associate Role – Street Of …

Ensure you are able to go through this exercise fairly rapidly and without the help of Excel or a calculator. Clearly state the simplifying assumptions you are making and their ramifications. * The group is thinking about the purchase of a company on the 31st of December of Year 0; * Entry several: 6.0 x LTM EBITDA; * Entry Financial obligation quantum: 3.0 x LTM EBITDA; * Assuming no financing and deal costs; * Rates of interest for the debt worked out at 5%; * Debt paid back as a bullet at the end of the investment period; * Sales: $100m in Y0, growing at 10% year-over-year (y-o-y) for the next 5 years; * EBITDA: historical margin at 40% of Sales; * Depreciation & Amortization: $30 million annually, steady; * Capital Expense: 15% of Sales; * Net Working Capital (NWC) requirements anticipated to increase by $2 million each year; * Minimal tax rate of 25%; * Exit at the very same entry EBITDA multiple, after 5 years.

Particular funds can have their own timelines, financial investment objectives, and management philosophies that separate them from other funds held within the exact same, overarching management firm. Effective private equity firms will raise lots of funds over their lifetime, and as firms grow in size and intricacy, their funds can grow in frequency, scale and even uniqueness. To get more info regarding securities exchange commission and also - visit the videos and -.

Prior to establishing Freedom Factory, Tyler Tysdal handled a growth equity fund in association with several celebrities in sports and entertainment. Portfolio business Leesa.com grew quickly to over $100 million in earnings and has a visionary social objective to “end bedlessness” by donating one mattress for each 10 offered, with over 35,000 contributions now made. Some other portfolio business remained in the markets of wine importing, specialized financing and software-as-services digital signage. In parallel to handling properties for organisations, Tysdal was managing personal equity in real estate. He has had a variety of effective private equity financial investments and a number of exits in student housing, multi-unit housing, and hotels in Manhattan and Seattle.

1. Deal metrics Start by determining the firm value at entry, the financial obligation quantum, and deduce the equity acquisition price. Sales for Year 0 were $100m with an EBITDA margin of 40%, which provides an LTM EBITDA of $40m and for that reason an entry Firm Value of $240m. The quantum of debt is figured out in a similar method, offering $120m.

Other job interviewers will give a leverage ratio rather of a financial obligation multiple; the debt is then computed directly from the Firm Worth. 2. grant carter obtained. Sales and EBITDA Use growth and margin assumptions to determine the Sales, then EBITDA, for every single year. Do not think twice to ask your job interviewer if rounding is acceptable; it will save you a great deal of time, show that you are fully knowledgeable about the approximation you are making, and offers excellent outcomes. https://player.vimeo.com/video/445058690

Interests & taxes Apply the interest rate provided to the Debt small total up to determine the yearly interest cost. Taking out the interest cost from the EBITDA causes the EBT, from which taxes are determined. This then leaves us with the Net Income. 4. Cash streams The objective here is to come up with the money streams readily available for financial obligation repayment for every year.

Glossary Of Private Equity Terms

Given that D&A is a non-cash expenditure, it ought to be included back in. 5. racketeering conspiracy commit. Firm Value at exit Using the exit numerous to the year 5 EBITDA, we come up with the exit Firm Value. The financial obligation at exit is the debt at entry, minus the cumulative money flow available for debt payment.

6. Money numerous and IRR The cash several (also called cash several) is specified as the ratio of exit to entry equity. The IRR is the yearly return of the investment. This often needs a calculator, however, a few estimated figures are worth remembering, e.g. a cash multiple of 3x over 5 years is comparable to a 25% IRR.

Now, repeat this exercise with just a pen and paper and develop new sets of presumptions. Train and train again until you have the ability to do all this by heart and relatively quickly. For mode practice, examine out our private equity case research studies and modelling tests here. Now, repeat this exercise with just a pen and paper and create brand-new sets of presumptions.

For mode practice, examine out our private equity case studies and modelling tests Earnings: Smart Gaming Ltd establishes games for smart device users. private equity fund. The primary item is cost 19.90 per download (this is a one-off cost). The business offered 1.5 million copies in 2011 (the first year it started trading) and 2.5 million copies in 2012.

How Private Equity Works, And Took Over Everything

Every video game offered creates an additional 5 revenue per year (i.e. in-game items and advertising) which is recurring and increases by 20% every year. However, just 30% of the users keep the app on their smart device every year (that is, only 30% of the previous year user base keeps using the item) – investment fund manager.

Therefore, private equity companies can afford to be very requiring and small mistakes can prove to be deadly in private equity interviews. Altough this might sound basic, an extremely common mistake of private equity interview prospects is to forget to do proper research study on the fund they are talking to with.

Fair concerns might include “which deal do you like a lot of and why”, “which deal do you like the least”, “why do you think we purchased XXX”, and “have you check out about our most current deals”. Make sure you comprehend the financial investment thesis for at least 3 of them, check out press short articles and any other source of information you can find.

Similarly, if you understand a lender or expert that worked on the deal, attempt to gather some details. Well informed and prepared candidate constantly impress, and unprepared candidates will seem not inspired. Another fair concern in private equity interviews is “do you have any investment concepts for us?” – million investors state. This is a very standard concerns and I would recommend to prepare at least 2 ideas (ideally 3) that are well developed and believed out.

What Private Equity Firms Need To Know About Data .

You will not be anticipated to understand all the details, however you will be anticipated to understand the investment reasoning, some key financials, some industry trends and why you believe it would be a good suitable for the fund. Normal error include having too broad ideas (i.e. I think a bank would be an excellent financial investment), or something innapropriate for the fund (since of size, geography or sector, for instance).

If you are a lender or specialist, you will be expected to learn about any transaction you worked on in terrific information (particularly for the current ones). Rationale, financials, deal specifics, structure, process, rates of financial obligation instruments, your precise role in the deal, and so on. Anything that is not private might potentially be asked.